Natera, Inc.

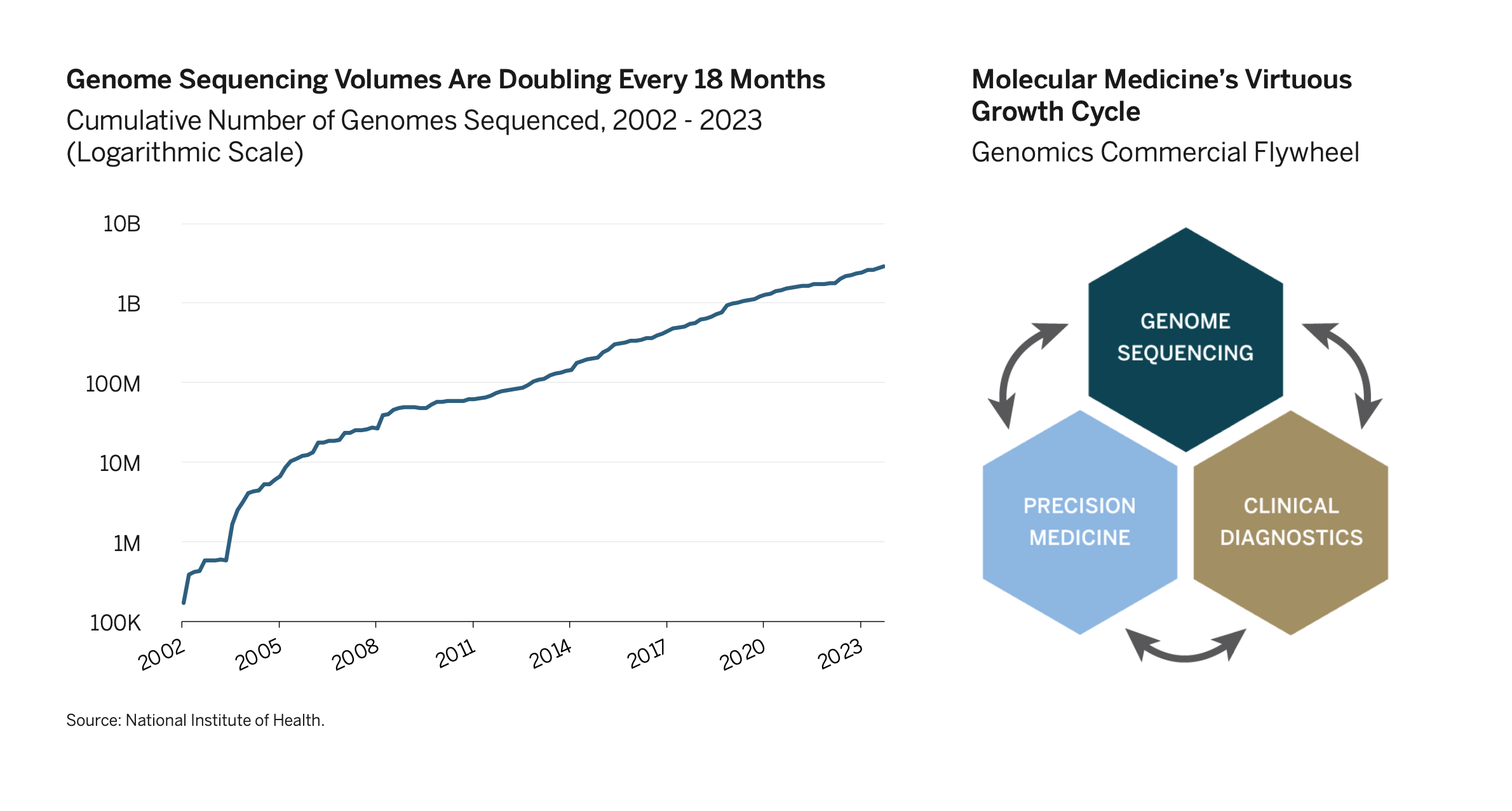

During the first quarter, we initiated a position in Natera, Inc. (NTRA), a global leader in genetic testing for women’s health, oncology, and organ health, as part of our Advent of Molecular Medicine theme. NTRA is the market leader in non-invasive prenatal testing (NIPT) and is pioneering minimum residual disease (MRD) testing methods to detect recurrence in cancer patients after initial treatment. We believe NTRA is well-positioned to capitalize on their strong position in women’s health, clear value proposition and growth potential within the oncology space, and proprietary IP and clinical data.

Accenture Plc

During the first quarter, we initiated a position in Accenture Plc (ACN) as part of our Heterogeneous Computing theme. One of the largest information technology services consulting firms in the world, ACN has diverse revenue streams through a collection of business lines, which include business process outsourcing, IT services, and cloud services. We believe ACN will benefit from the growing need for the guidance and integration services required to strategically position companies in the evolving landscapes of cloud computing, artificial intelligence, and other next-gen infrastructure.

Atmos Energy Corporation

During the first quarter, we initiated a position in Atmos Energy Corporation (ATO), within the balance portion of our portfolio. Atmos is the largest pure-play natural gas distribution company in the U.S., serving customers across eight states. We believe Atmos will continue to drive organic revenue growth in coming years, supported by favorable population demographics in their service areas, a supportive regulatory environment, and strong balance sheet. Furthermore, as a fully regulated natural gas delivery platform, ATO provides diversification relative to our other investment in electric utilities.

American Express Company

During the first quarter, we initiated a position in American Express Company (AXP), as part for our Post-Pandemic Consumer theme. AXP is a best-in-class credit card issuer, lender, and payments processor. AXP’s high-quality client segments and premium cardholders give them exposure to increased leisure spending and an affluent customer base. In addition to having superior brand recognition, AXP’s valuation is currently undemanding relative to the market multiple.

Splunk Inc.

During the first quarter, we exited our position in Splunk Inc. Splunk, a cybersecurity and observability company, had been a holding in our Heterogeneous Computing theme since 2018 and was acquired Cisco Systems Inc. (CSCO).