Fourth Quarter, 2023

Click here for a printable version of the Investment Update.

Click here to listen to an audio version of the Investment Update.

Strong equity market performance in 2023 has many investors entering 2024 optimistic about the economy and markets. While we see risks in the broader market, we also see neglected investment opportunities at home and abroad.

A Year That Defied Expectations

After the poor performance of most major financial markets in 2022, investors and market strategists entered 2023 expecting a recession and negative market returns. In fact, for the first time in at least two decades, investment strategists polled by Bloomberg predicted negative returns for the S&P 500 in the year ahead.

There was good reason to be gloomy. As of January 2023, the Federal Reserve had raised its target policy rate from 0%- 0.25% in March 2022 to 4.25%-4.50% and was signaling more rate hikes ahead. It seemed a near certainty that the largest string of rate hikes since 1979 would have a decidedly negative impact on economic growth and market returns.

Yet equity markets defied expectations, in response to better-than-expected economic growth and corporate earnings. The S&P 500 delivered a 26.3% total return, which the EuroStoxx 50 almost matched at 23.2%. Japan’s Nikkei 225 did even better, returning a whopping 30.9%. Many emerging markets also posted strong gains.¹

Bond markets, by contrast, had a wild ride. Inflation and Fed policy worries drove the highest volatility since the Global Financial Crisis. After soaring to its highest level since 2007, the yield on the 10-year U.S. Treasury Bond finished 2023 within one basis point of where it started.

Pundits have offered many explanations for why the Fed’s rate hikes didn’t slow economic growth as expected, including the following:

▪ Excessively easy fiscal policies offset tight monetary policy.

▪ The aging population and widespread deleveraging made consumers and businesses less sensitive to rising interest rates.

▪ The economy was simply returning to normal after the convulsions of the pandemic (see sidebar).

▪ It takes time for rate hikes to slow the economy, and we have yet to see their full impact.

▪ The aging population and widespread deleveraging made consumers and businesses less sensitive to rising interest rates.

▪ The economy was simply returning to normal after the convulsions of the pandemic (see sidebar).

▪ It takes time for rate hikes to slow the economy, and we have yet to see their full impact.

All four of these explanations may be true to some degree. We see a path for the soft-landing investors have now come to expect, but this is not our base case. We think the most aggressive monetary policy tightening in 40 years is likely to slow the economy. While this has not happened yet, consumer spending is slowing, often a signal of a broader slowdown ahead.

Looking Ahead

The Wall Street consensus now is that the Fed will cut rates by 1.5% in 2024. Polling suggests most investors expect a soft- landing, in which inflation cools without a recession or a spike in unemployment. This widespread rosy narrative could set the stage for unwelcome surprises that may trigger a selloff in 2024, just as the widespread gloom of a year ago set the stage for positive surprises to trigger 2023’s big rally.

We see several potential negative surprises that could trip up the market in 2024. Most notably:

▪ Disappointing top-line sales and corporate profit margins could lead to slower-than-expected earnings growth, or

▪ Lackluster results from the so-called Magnificent Seven could lead to a repricing of these mega-cap stocks.

▪ Lackluster results from the so-called Magnificent Seven could lead to a repricing of these mega-cap stocks.

Profit Margins

The sharp rebound in profit margins has surprised many investors. After margin declines in 2022 and early 2023 driven by higher costs for labor and other inputs, investors expected continued weakness in the second half of last year. However, management teams focused maniacally on efficiency and beat these expectations. Today, consensus earnings projections call for S&P 500 profit margins to expand further in 2024² and remain well above their historically high average of 10.9% from 2012 to 2019.

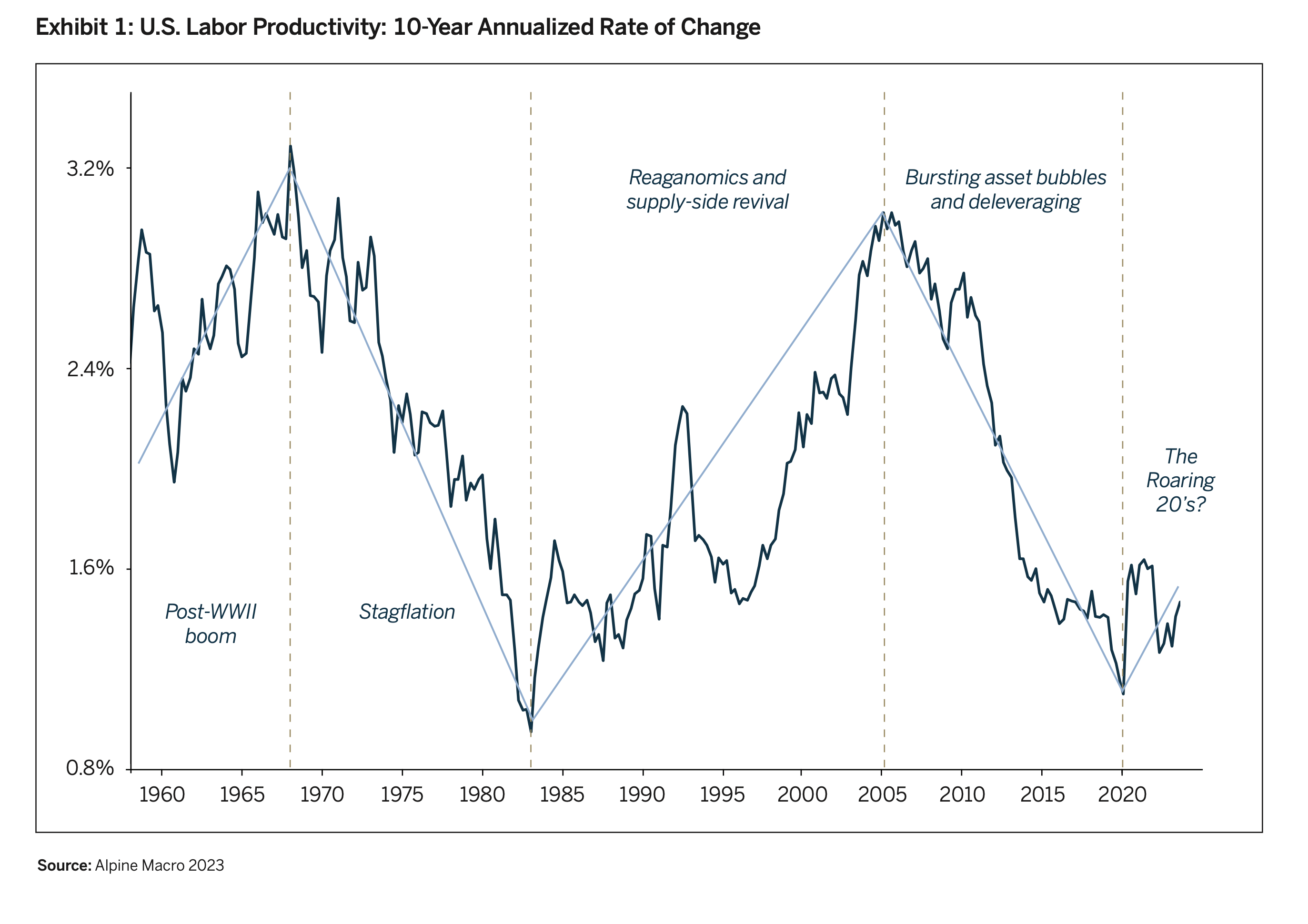

Some bulls attribute the recent strong growth in profit margins to improving labor productivity, which goes through long waves, with wars or major crises often acting as inflection points (Exhibit 1). Optimists suggest the 2020 pandemic was the much-needed catalyst to push the U.S. economy out of a long decline in productivity and income growth. It’s possible. For example, there has been a five-fold increase in working from home since the pandemic began. Recent research has found that working three days a week in the office and two at home does not reduce productivity and allows firms to save on recruitment and employee retention costs.

We are big believers in productivity improvements and eagerly embrace inventiveness. Most of our themes encompass disruptive innovations that improve productivity. Nonetheless, profit margins seldom rise in a straight line, even during productivity booms. We think it is unlikely that margins can continue to expand at their recent pace much longer. Other factors that have pushed margins higher — globalization, downward wage pressure, low interest rates and falling tax rates — appear to be exhausted. We are thus skeptical that earnings will rise at the double-digit rate that the consensus now projects for 2024, especially if inflation continues to fall and companies cannot raise prices.

The Magnificent Seven

There’s another reason we are skeptical of continued broad strength in profit margins and returns. Both depend on continued strength for the S&P 500’s seven largest companies by market capitalization: Apple, Microsoft, Amazon, Nvidia, Alphabet (Google), Meta (Facebook) and Tesla. Together, these stocks delivered over 60% of the Index’s return in 2023— and each of them gained more than $300 billion in market capitalization, more than the total market cap of all but 20 names in the Index.

Remarkably, these stocks widened their return leadership in 2023. The market weight of the top seven names is now 28%, magnifying the impact of their returns, margins and valuations on the Index.

For the past decade, superior products and business strategies have driven rapid sales and earnings growth for the Magnificent Seven. But the most recent data suggest that sales growth for these companies is now running no faster than nominal GDP growth. In addition, government pressures in Europe and the U.S. are beginning to erode their monopolistic positions and pricing power.

This is concerning. Expectations of continued rapid sales and earnings growth—and fear of betting against a juggernaut— have led almost every class of investor to have significant exposure to these companies. As a result, each appears to be somewhere between fully priced and extremely expensive. Given their outsize weight in the S&P 500, disappointing results for these widely-held and richly-valued stocks could drive a decline in the Index.